Steve Bruns, MPP, Staff Writer, Brief Policy Perspectives

Balancing the tradeoff between access and affordability is a key challenge of enacting reform in the health insurance marketplace. Policies designed in good faith to improve the market must consider how to increase access to care for sick, high-cost individuals while maintaining affordability for all.

A recently proposed rule from the Department of Labor (DOL) attempts to strike no such balance between these competing interests. The agency’s proposal would allow small businesses to create less stringently regulated health plans that benefit healthier workers seeking cheaper, less comprehensive care, however, these plans would come at a significant cost to people with serious, more expensive health needs. While policy options that increase access while protecting affordability do exist, DOL’s proposal is not one of them.

The proposed rule, authorized by an October 2017 Executive Order, expands the conditions under which small businesses can band together to create an Association Health Plan (AHP). Under current law, self-employed and small businesses (those with fewer than 50 employees) must purchase insurance on the individual and small group marketplaces, respectively. Affordable Care Act (ACA) rules govern these markets, requiring, for instance, that coverage include essential health benefits such as hospitalizations, prescription drugs, and emergency care. Under the proposed rule, self-employed and small businesses could band together to create associations based on operating in the same industry or the same geographic region. Such associations could create their own health plans, AHPs, which could be offered in the large group marketplace and therefore be exempt not only from ACA rules but also from most state-level regulations.

The rule purports two key benefits. First, operating in the relatively deregulated large group market will allow AHPs to offer less comprehensive, more affordable plans for employers with younger, healthier employees. Second, AHPs will allow small businesses to join a larger, more balanced risk pool with lower and more predictable costs.

In practice, however, third party analyses predict that the proliferation of AHPs will destabilize the individual and small group markets and ultimately drive up costs for older, sicker individuals. The relaxed regulatory environment for AHPs provides a clear incentive to market health plans to younger, healthier people, luring them out of the ACA-governed markets and leaving behind an older, sicker, and costlier risk pool. In short, the healthy win and the sick lose.

Yet those who choose to join an AHP will do so at their own risk. For instance, a small business with relatively healthy employees may choose to join an AHP, but an employee who contracts a serious illness requiring comprehensive care—such as cancer or HIV—may find that the plan does not provide the care that they need. Thus, once sick, previously healthy AHP participants will likely re-enter the ACA markets, where they will contribute to and contend with the problem of rising costs. For those who manage to stay healthy enough for an AHP to remain attractive, they may still not receive adequate benefits. AHPs are historically rife with fraud and insolvency. During a cycle of scams in the early 2000s, 144 fraudulent operations selling coverage through AHPs left over 200,000 policyholders with over $252 million in medical bills

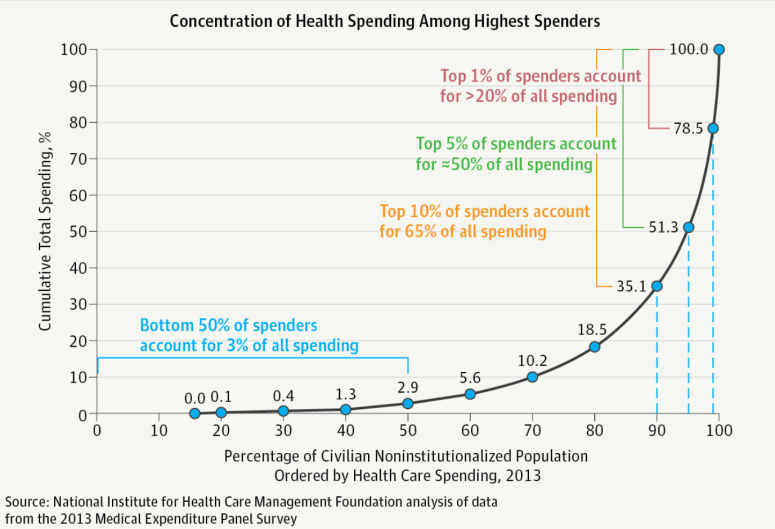

From a broad perspective, the proposed rule ignores a demographic reality. The distribution of health risk and spending in the U.S. mirrors the 80-20 rule: 20% of the population accounts for 80% of the total costs.

Financing care for the sick is an inevitability, whether it is in the form of healthy individuals paying higher insurance premiums, patients paying higher costs to providers who administer uncompensated care to high-cost patients who are unable to pay their own bills, or public subsidies financed by taxation. AHP expansion thus merely shifts premium costs from the healthy to the sick and tucks any remaining costs—such as those incurred by the sick who are priced out of insurance—into taxes and providers’ prices.

The ACA attempted to finance care for the sick using a market-based approach that required healthy, lower cost individuals to participate in the same risk pool as sick individuals or pay a tax penalty. With the individual mandate now repealed and the proposed AHP rule potentially in effect soon, those efforts to create a larger, balanced, and inclusive risk pool are being reversed.

The current administration would be wise to avoid taking this step backward and instead incentivize the healthy to participate in the same risk pool as the sick. Finalizing the AHP rule would be a misstep, treating a symptom in the market without addressing the underlying cause.

2 thoughts on “Proposed rule would expand association health plans at the expense of the sick”