The following is an op-ed and does not necessarily reflect the views of Policy Perspectives or the Trachtenberg school.

Madison Grady, MPP Staff Writer, Brief Policy Perspectives

In the midst of the novel coronavirus (COVID-19) pandemic in the United States, policy experts have been weighing in on ways the government can soften the extensive economic harm facing society. Right now, unemployment, supply chain failures, profit loss, and impacts of quarantining are some of the biggest harms. In response to these challenges, Congress passed the Coronavirus Aid, Relief, and Economic Security (CARES) Act on March 27, 2020. Part of the plan details handing out an average of $1,200 to every adult American each month, depending on their income. This type of policy is colloquially known as helicopter money because it seems to fall from the sky and is part of the stimulus package that totals up to $2 trillion.

Helicopter money is handed out via a refundable tax credit, meaning citizens will receive the money even if they don’t owe income taxes because their income is too low. During some of the United States’ hardest times, policymakers have used helicopter money in different ways to help stimulate the economy. In the 2008 recession, Congress passed the Economic Stimulus Act of 2008, which provided large tax cuts to most households. Individuals received a basic credit of up to $600 ($1,200 for joint filers) between May and July. While Congress passed the act in February of 2008, it took three months for the policy to go into effect.

The 2008 stimulus passed by President George W. Bush totaled approximately 1% of the gross domestic product (GDP), and economists agreed that the bill would immediately increase consumer spending. However, taxpayers did not receive the checks until mid-summer, and by that time, it was too late to affect the first half of the year. Even if the checks had arrived on time, the extra money would not have done much for the economy because tax rebate checks are not an efficient way to stimulate the economy. Due to the low spending propensity, the rebates in 2008 provided little in economic stimulus. Many taxpayers saved the money or used it to pay off debts. This helped some consumers’ well-being during the crisis, but it did not make them spend, which is what the rebate was meant to do.

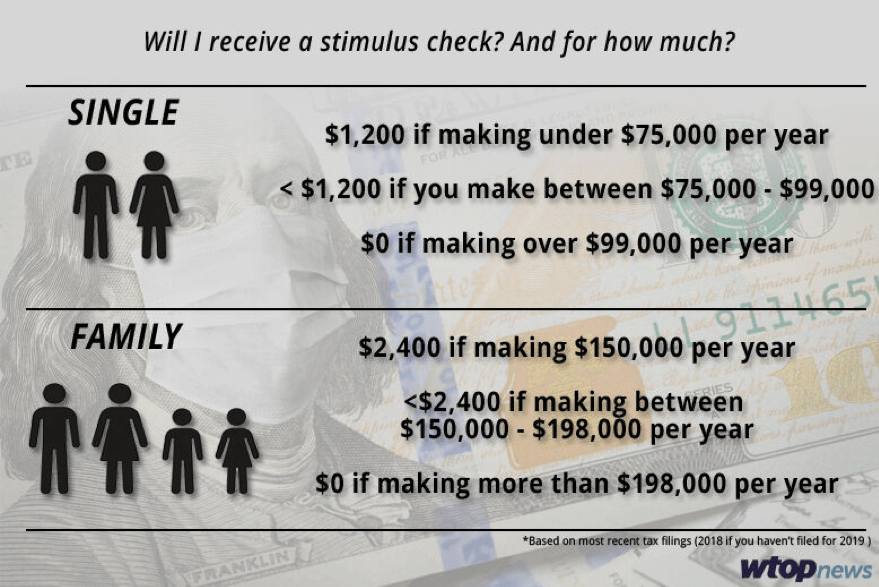

What is being proposed now to combat the COVID-19 panic needs to be continuous and would need to last for the duration of the crisis, explains David Beckworth, an economist at George Mason University. This means that a one-time payment isn’t going to be enough to meaningfully impact the economy. The CARES Act, put forth by Senate Republicans, gives a one-time payment to individuals up to $1,200 ($2,400 for joint tax filers).

Additionally, families will receive $500 for each child. If an individual’s income exceeds $75,000, the stimulus check they receive will be reduced by 5% of the amount their income exceeds that threshold. The Internal Revenue Service (IRS) will use 2019 tax returns (or 2018, if 2019 has not yet been filed), Social Security benefits, and Railroad Retirement benefit statements to determine the amount owed. If economic conditions do not improve, Congress has discussed the idea of distributing a second stimulus check later this year.

The biggest argument in favor of the tax credit plan is that it bypasses the usual red-tape laws of monetary policy. As major parts of the economy are shutting down in an effort to slow the spread of COVID-19, it would be the best way to ensure that every American without work gets some relief. Helicopter money is a direct injection of cash into the economy, if taxpayers choose to spend it, and could lead to an increase in demands for goods.

However, Michael Tanner of the Cato Institute points out that this policy would only help those who don’t need it. Most Americans right now either aren’t missing a paycheck or are already eligible for existing programs such as unemployment insurance. Americans who are low-income or vulnerable households will struggle to receive a payment. Workers who earn less than the standard deduction of $12,200 ($24,400 for joint filers), or those who don’t report their cash income most likely didn’t file a 2018 or 2019 tax return and therefore will not receive a payment. Dependents over the age of 17, including cared-for parents or disabled children, will also not receive a direct payment, and their caretakers will not receive a benefit for them. The policy also excludes anyone without a Social Security number, including Deferred Action for Childhood Arrivals (DACA recipients) or citizens with only Individual Taxpayer Identification Numbers (ITIN). Lastly, the likelihood of the government being able to administer the program quickly is slim, and checks could arrive months from now, just as in 2008.

The current plan to give a one-time stimulus check to taxpayers has greater implications for the future. First, once this policy goes into effect, it opens the door for politicians and other government agencies that want to give out helicopter money like this all the time and increases the feasibility of Universal Basic Income plans. The current policy of handing out money could be repeated until the government thinks it’s making a difference in the economy – without any data or indices to support that belief. The plan needs to be tied to an economic indicator, such as national GDP. Second, economic relief packages that create money can also raise inflation. When there is too much money in the system, prices start to go up. While the nation is unlikely to see inflation in the short term, a cash stimulus can have long-term effects. However, proponents agree that some inflation in the long term is worth it if it helps people today.

The ramifications of COVID-19 have had dramatic impacts on consumer spending patterns: citizens are quarantined in their homes; businesses, restaurants, and bars have shut down; and travel restrictions have fundamentally changed movement patterns. A check from the government is not going to help solve long-term problems or make people spend more money. In hoping to provide citizens with a lifeline during this hard time, Congress hastily passed a plan that excludes our most vulnerable populations and those who truly need help right now. Political leaders on both sides of the aisle need to recognize that helicopter money is a bandaid, not the solution to the economic challenges facing Americans today. When the stimulus checks do not solve the economic problem, policymakers need to be prepared with additional stimulus plans that address the likelihood of what could be a long-lasting recession.

One thought on “Op-Ed: Helicopter Money Is Not the Solution to the COVID-19 Panic”