Steve Bruns, MPP, Staff Writer, Brief Policy Perspectives

In 1977, Bert Lance, director of the Office of Management and Budget under President Jimmy Carter, urged the federal government to operate using a simple motto: “If it ain’t broke, don’t fix it.” Lance explained, “That’s the trouble with government: Fixing things that aren’t broken and not fixing things that are broken.”

The Affordable Care Act (ACA), also known as Obamacare, could well be one of those things.

In the first two months of 2017, the 115th Congress has oscillated between plans to “repeal and delay,” “repeal and replace,” and simply “repair” the ACA. No matter the name, any plan to reform the health care law should heed Lance’s advice: protect the parts of the law that are working and focus on the aspects in need of repair.

So, what’s working and what needs fixing?

Though the law is complex, the ACA’s two main policy goals are simple: increase access to healthcare and reward the delivery of high-quality, not high-quantity, care. Current data show the law has made demonstrable progress in reaching both goals. First, the ACA intended to increase access to healthcare by enacting several key provisions:

- Expanding Medicaid eligibility to cover groups previously left out of public health coverage, such as low-income families, able-bodied parents, low-income adults without children, and many low-income individuals with chronic mental illness or disabilities.

- Creating a new insurance marketplace where Americans can shop for coverage, some with financial help from the federal government.

- Requiring that all Americans carry health insurance coverage or pay a tax penalty, otherwise known as the individual mandate.

- Allowing young adults to receive coverage through a parent’s plan through age 26.

- Barring insurance companies from denying coverage based upon a pre-existing condition.

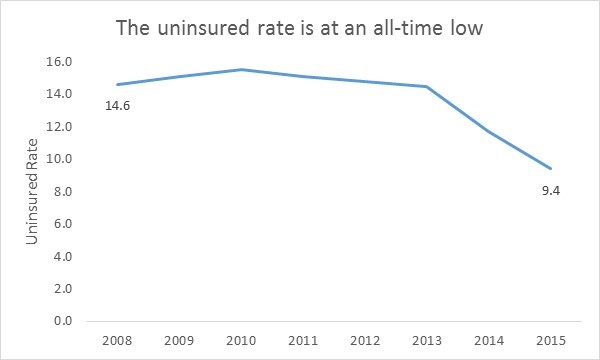

Fully enacted in 2014, these provisions resulted in historic gains in health coverage that brought the uninsured rate to an all-time low. Between 2013 and 2015, the number of uninsured fell from 41.8 million to 29.0 million – a drop of 12.8 million and 5.2 percent.

The ACA increased insurance coverage everywhere and among every demographic group. However, these facts are not clear to everyone. Just a quarter of the population knows that the uninsured rate is at an all-time low, and only 49 percent of Republicans believe the ACA has increased health coverage.

Surprisingly, this fairly massive insurance expansion, financed by tax increases for wealthy households and Medicare cuts, actually saves money for the federal government. In 2012, the Congressional Budget Office estimated that the ACA will save $109 billion over the next decade.

The ACA also intended to transform the healthcare financing system from one that pays for the volume of services to one that rewards providers for delivering higher-quality care. In the current quantity–over–quality system, providers routinely deliver unnecessary services and procedures that do not improve patient outcomes. In fact, a study from the Institute of Medicine estimated that in 2009, 30-40% of healthcare spending went toward activities and procedures that are essentially unnecessary and unhelpful for a patient’s health.

To buck this trend, the ACA created several alternative payment models that tie payments to value, incentivizing quality and efficiency of care, rather than quantity. For instance, Accountable Care Organizations (ACOs) bring hospitals and physicians together in a structure where providers are paid to avoid unnecessary care, reduce errors, and keep Medicare beneficiaries out of the hospital. The ACO program is still new, but the results are showing improved quality with a small, but meaningful, reduction in the overall cost of care. Many other payment reform efforts have only recently begun, so it’s too soon to say whether they might curb spending. However, the underlying emphasis on rewarding quality of care is essential for a country that spends far more on health care than other developed nations but has worse health outcomes.

Despite making notable progress, the ACA does have flaws that require fixing. In particular, insurers in the ACA marketplace have struggled to earn profits, and patients are contending with rising premiums and deductibles. A McKinsey report found that in 2014, insurers lost about $2.7 billion covering ACA beneficiaries and likely more than that in 2015. With financial losses mounting, major carriers—such as Aetna, Humana, and UnitedHealth Group—no longer sell coverage in the ACA marketplace. In an attempt to recover lost profits, insurers still participating in the marketplace have increased their premiums by an average of 25% in 2017 compared with 2016.

To correct these disruptions in the market, policymakers should first ensure that healthy people sign up for and maintain coverage. The ACA requires that insurers cover patients regardless of preexisting health conditions. Sicker beneficiaries cost insurance companies more money, and healthier patients balance out these costs. However, insurers have had trouble signing up enough young, healthy, and profitable adults to offset the older, sicker patients – whose high medical costs they’re legally required to cover.

As it stands, healthy people can opt in and out of insurance coverage with relative ease. A recent analysis by the Kaiser Family Foundation found that more than seven million people eligible for exchange coverage would pay less in penalties than for the least expensive insurance option available to them. One obvious solution is to strengthen the penalties for everyone, including healthy people, for not carrying insurance and require that people maintain coverage for an entire year. Or, the government can provide larger subsidies for healthy people to purchase coverage. Adding healthier patients to the risk pool would help insurers better predict the yearly cost of coverage, potentially stemming the growth in ACA marketplace premiums.

To further balance the risk pool and reduce premiums, more states should expand Medicaid. There are 20 states that opted not to receive federal funding to expand Medicaid eligibility, a maneuver that pushed lower income and generally less healthy patients into the ACA marketplace, skewing the overall risk pool to include more expensive patients. Insurance companies tend to ask for higher premiums in states where policymakers declined to expand Medicaid—marketplace premiums are about 7% lower in expansion compared to non-expansion states. There is also a significant gap in uninsured rates between states that expanded Medicaid and states that did not: numerous analyses demonstrate that Medicaid expansion states experienced large reductions in uninsured rates and that these reductions exceed those in non-expansion states. Additional estimates predict that expanding Medicaid nationwide would provide coverage to three million more people.

Current congressional proposals threaten to roll back the ACA’s progress. Nearly 18 million people could lose their insurance if the ACA is repealed with no replacement, according to the Congressional Budget Office. Moreover, the proposals share a set of elements that would ultimately reduce insurance premiums but increase consumers’ out-of-pocket costs by an average of $1,744 per year. The impact would be larger for older patients, ages 55 to 46, whose total costs would increase by $6,089 annually.

Rather than repealing and moving backward, a more responsible reform would at least incentivize younger, healthier people to obtain and maintain insurance coverage and guarantee coverage for lower income, less healthy patients eligible for Medicaid. Together, these two reforms alone could increase coverage, reduce premiums, and stabilize the ACA marketplace while protecting a system designed to improve the quality of care that all Americans receive, both inside and outside of the ACA marketplace.

In other words: if it ain’t broke, don’t repeal it. Fix it.

One thought on “If it ain’t broke, don’t repeal it”