Jessica Blackband, MPP, Staff Writer, Brief Policy Perspectives

![]() Reporting on Hurricane Harvey’s aftermath has died down, but the 82,000 people who filed flood insurance claims after the disaster are still awaiting relief. These homeowners, developers and property managers are covered under the National Flood Insurance Program (NFIP), a FEMA program that subsidizes insurance premiums for these groups. The program has been criticized for creating a moral hazard, explained below, and failing to incorporate the influence of a changing climate on flood risk. There is a strong environmental and economic case to be made for restructuring the program.

Reporting on Hurricane Harvey’s aftermath has died down, but the 82,000 people who filed flood insurance claims after the disaster are still awaiting relief. These homeowners, developers and property managers are covered under the National Flood Insurance Program (NFIP), a FEMA program that subsidizes insurance premiums for these groups. The program has been criticized for creating a moral hazard, explained below, and failing to incorporate the influence of a changing climate on flood risk. There is a strong environmental and economic case to be made for restructuring the program.

Economic and Environmental Challenges for the NFIP

Established in 1968, the NFIP subsidizes flood insurance for homeowners and small businesses that own property in flood-prone areas. Although it makes flood insurance cheaper and more widely available, it also creates a moral hazard by incentivizing developers to build and sell property in areas likely to flood, which poses a large financial risk. As a result, taxpayers take on the cost of building and repairing properties in flood-prone areas, not the individual home buyers and sellers.

Another central issue with the program is that it disproportionately favors a small number of properties. 11,000 highest risk properties, or severe repetitive loss properties, receive almost 30 percent of the disbursements. Many of these homeowners would be willing to relocate instead of rebuilding, but currently flood insurance policies only cover repairs to existing property or flood mitigation enhancements.

A variety of environmental factors exacerbate the program’s challenges. Due to sea level rise, the number of communities impacted by repeated flooding events in the U.S. could double by 2060. Heavy precipitation events are also expected to occur more often in the coming decades than they have in the past, thanks in large part to climate change. Although a direct relationship between increased flooding and climate change has not been established, more frequent heavy precipitation events could certainly contribute to more flood events.

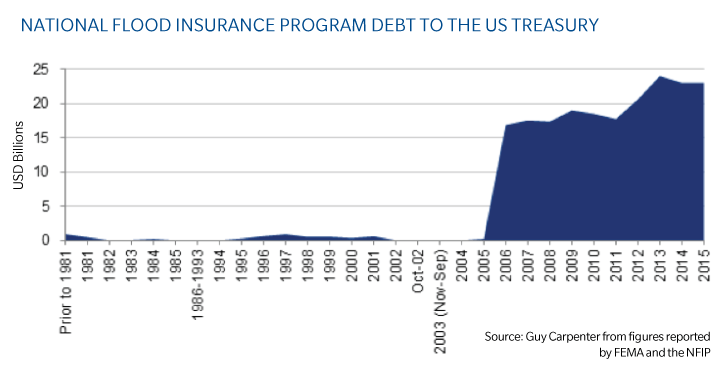

Despite the structural challenges and increasing frequency of flooding, the Senate passed a bill last month to forgive more than half of the program’s $30 billion in debt. The NFIP needed the bailout to cover the claims from this summer’s natural disasters; as mentioned, more than 80,000 claims were filed in the wake of Hurricane Harvey alone.

Reforming the NFIP

The policy community is well aware of the negative incentives created by the NFIP and experts have proposed a variety of fixes. Policymakers could raise premiums to incorporate the rising risk associated with higher sea levels and heavily populated floodplains. This would likely be unpopular, and FEMA has not started accounting for sea level rise projections in its flooding risk assessments. The Natural Resources Defense Council (NRDC) suggested making the program’s payout stipulations more flexible by allowing insured homeowners to sell their homes and relocate, rather than rebuilding. Others suggest privatizing the market so that homeowners bear the full risk of floods on their property.

Given the recent disasters and urgent need for reform, the NFIP has drawn attention and criticism from across the political spectrum. Environmental groups like the NRDC and the Center for Biological Diversity have publicly condemned the program in its current form. Public opinion doesn’t favor the program, either; a poll conducted by the Pew Charitable Trust found that 75 percent of voters would prefer to see FEMA buy severe repetitive loss properties in flood-prone areas, and 82 percent support mandatory flood preparedness requirements for public property.

Impediments to Reform

Although there is widespread support for reform, more than half of the households covered by the program are in heavily populated, and politically powerful, Texas, Louisiana, or Florida, which may be causing gridlock on reform measures in Congress. It is also possible that program reform attempts have been caught in the politically charged debate over climate change. Politicians who are not convinced that the impact of climate change will be drastic may be more hesitant to take action to prepare for its future effects. Finally, there is usually more political will for disaster response spending than disaster preparedness spending.

With every new natural disaster, the NFIP is swept up in a tide of controversy, but a variety of promising policy solutions are on the table. It seems likely that the escalating cost of natural disasters in the United States may finally prompt substantial reform of the program, and policymakers should integrate some of the innovative reforms devised to strengthen the NFIP when the program comes up for renewal in December. Particularly in coastal areas, the landscape of risk is rapidly changing; at a bare minimum, a reauthorized NFIP should integrate the growing risks to people and property posed by sea level rise and flooding.